Will Rising Taxes Decimate Your Retirement?

FINANCE

Bruce Reimer

There are few things more painful than writing a big check to the Tax Man. Every dollar you send him was earned using your irreplaceable life energy and represents one less dollar for you to spend or save.

How much you pay the Tax Man can mean the difference between a new car or continuing to drive the one you own. It can dictate where you take a vacation and the amenities you can afford. It can change the options you can offer your children for education. How much you pay the Tax Man can change your quality of life.

For this reason, tax-deferred investments such as IRAs, 40Iks, “tax-free” municipal bonds are very attractive to the average wage earner. By investing in these vehicles and “avoiding” the tax, you have a chance to squirrel away more income for retirement or a rainy day... or do you?

While this may sound like a good idea right now, is it going to put you ahead of the money game in the long-term? The answer is “It depends.”

You see, just how sound this strategy is depends on:

Tax rates now and tax rates when you access those funds in the future.

Let’s take a look at an example so you can see what I mean. Let’s compare investing in a:

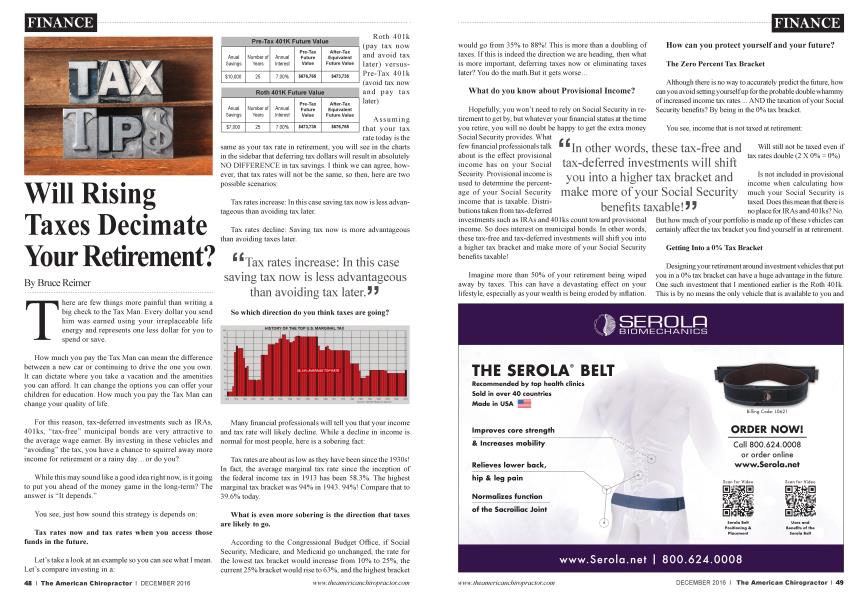

Pre-Tax 401K Future Value After-Tax Anual Number of Annual Equivalent Savings Years Interest Future Value $10,000 25 7.00% $676,765 $473,735 Roth 401K Future Value After-Tax Anual Number of Annual Equivalent Savings Years Interest Future Value $7,000 25 7.00% $473,735 $676,765

Roth 401k (pay tax now and avoid tax later) versusPre-Tax 401k (avoid tax now and pay tax later)

Assuming that your tax rate today is the

same as your tax rate in retirement, you will see in the charts in the sidebar that deferring tax dollars will result in absolutely NO DIFFERENCE in tax savings. I think we can agree, however, that tax rates will not be the same, so then, here aie two possible scenarios:

Tax rates increase: In this case saving tax now is less advantageous than avoiding tax later.

Tax rates decline: Saving tax now is more advantageous than avoiding taxes later.

^Tax rates increase: In this case saving tax now is less advantageous than avoiding tax later.??

So which direction do you think taxes are going?

Many financial professionals will tell you that your income and tax rate will likely decline. While a decline in income is normal for most people, here is a sobering fact:

Tax rates are about as low as they have been since the 1930s! In fact, the average marginal tax rate since the inception of the federal income tax in 1913 has been 58.3%. The highest marginal tax bracket was 94% in 1943. 94%! Compare that to 39.6% today.

What is even more sobering is the direction that taxes are likely to go.

According to the Congressional Budget Office, if Social Security, Medicare, and Medicaid go unchanged, the rate for the lowest tax bracket would increase from 10% to 25%, the cunent 25% bracket would rise to 63%, and the highest bracket

would go from 35% to 88%! This is more than a doubling of taxes. If this is indeed the direction we are heading, then what is more important, deferring taxes now or eliminating taxes later? You do the math.But it gets worse...

What do you know about Provisional Income?

Hopefully, you won’t need to rely on Social Security in retirement to get by, but whatever your financial status at the time you retire, you will no doubt be happy to get the extra money Social Security provides. What few financial professionals talk about is the effect provisional income has on your Social Security. Provisional income is used to determine the percentage of your Social Security income that is taxable. Distributions taken from tax-deferred investments such as IRAs and 40 Iks count toward provisional income. So does interest on municipal bonds. In other words, these tax-free and tax-deferred investments will shift you into a higher tax bracket and make more of your Social Security benefits taxable!

Imagine more than 50% of your retirement being wiped away by taxes. This can have a devastating effect on your lifestyle, especially as your wealth is being eroded by inflation.

^In other words, these tax-free and tax-deferred investments will shift you into a higher tax bracket and make more of your Social Security benefits taxable! 55

How can you protect yourself and your future?

The Zero Percent Tax Bracket

Although there is no way to accurately predict the friture, how can you avoid setting yourself up for the probable double whammy of increased income tax rates ... AND the taxation of your Social Security benefits? By being in the 0% tax bracket.

You see, income that is not taxed at retirement:

Will still not be taxed even if tax rates double (2 X 0% = 0%)

Is not included in provisional income when calculating how much your Social Security is taxed. Does this mean that there is no place for IRAs and 40 Iks? No. But how much of your portfolio is made up of these vehicles can certainly affect the tax bracket you find yourself in at retirement.

Getting Into a 0% Tax Bracket

Designing your retirement around investment vehicles that put you in a 0% tax bracket can have a huge advantage in the future. One such investment that 1 mentioned earlier is the Roth 401k. This is by no means the only vehicle that is available to you and

not the only place you should invest your money When designing your retirement, all factors must be considered. You must know how to allocate your funds so that you maximize the return on your wealth today and minimize the tax bracket that you find yourself in retirement. With effective planning, you can find yourself in a 0% tax bracket. Done improperly, you can end up paying a very stiff price for a seemingly smart idea today—deferring taxes. This is one piece of a bigger puzzle that each individual needs to solve. The help of a qualified professional can make the job relatively simple.

A Final Note

I

This is a rudimentary look at moving into a 0% tax bracket. Taxes are just ONE PIECE of a bigger puzzle that each individual needs to solve. There ai e many moving parts that make up a successful financial strategy. All factors and how they interrelate must be considered. Such as: How to systematically eliminate debt and simultaneously build wealth and manage cash flows to recover money that is slipping through the cracks in your practice. By simultaneously addressing repressive debt, taxes now and in the future, as well as lost practice profits, you can design your financial strategy to create the maximum amount of wealth hi the least amount of time. Those chiropractors who take this approach will predictably attract greater wealth.

Bruce Reimer,.Master Wealth Coach, at Chirowealth Learning Systems. Since 1979 has been an avid student of the markets, investing, risk diversification and tax law. You can reach him atwww.speaktobruce.com