The 3 Best Retirement Plans You Never Heard Of

FINANCIAL PLANNING

All my life, I've heard "there is nothing better than a 401K." That simply is no longer true.

John Medwin

The History of the 401K and Taxes

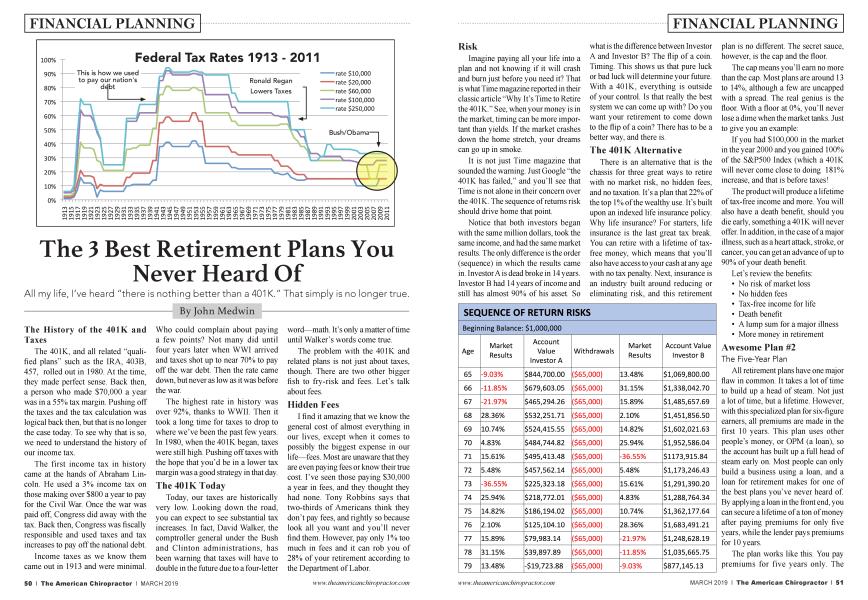

The 401K, and all related “qualified plans” such as the IRA, 403B, 457, rolled out in 1980. At the time, they made perfect sense. Back then, a person who made $70,000 a year was in a 55% tax margin. Pushing off the taxes and the tax calculation was logical back then, but that is no longer the case today. To see why that is so, we need to understand the history of our income tax.

The first income tax in history came at the hands of Abraham Lincoln. He used a 3% income tax on those making over $800 a year to pay for the Civil War. Once the war was paid off, Congress did away with the tax. Back then, Congress was fiscally responsible and used taxes and tax increases to pay off the national debt.

Income taxes as we know them came out in 1913 and were minimal. Who could complain about paying a few points? Not many did until four years later when WWI arrived and taxes shot up to near 70% to pay off the war debt. Then the rate came down, but never as low as it was before the war.

The highest rate in history was over 92%, thanks to WWII. Then it took a long time for taxes to drop to where we’ve been the past few years. In 1980, when the 40 IK began, taxes were still high. Pushing off taxes with the hope that you’d be in a lower tax margin was a good strategy in that day.

The 401K Today

Today, our taxes are historically very low. Looking down the road, you can expect to see substantial tax increases. In fact, David Walker, the comptroller general under the Bush and Clinton administrations, has been warning that taxes will have to double in the future due to a four-letter word—math. It’s only a matter of time until Walker’s words come true.

The problem with the 40IK and related plans is not just about taxes, though. There are two other bigger fish to fry-risk and fees. Let’s talk about fees.

Hidden Fees

I find it amazing that we know the general cost of almost everything in our lives, except when it comes to possibly the biggest expense in our life—fees. Most are unaware that they are even paying fees or know their true cost. I’ve seen those paying $30,000 a year in fees, and they thought they had none. Tony Robbins says that two-thirds of Americans think they don’t pay fees, and rightly so because look all you want and you’ll never find them. However, pay only 1% too much in fees and it can rob you of 28% of your retirement according to the Department of Labor.

Risk

Imagine paying all your life into a plan and not knowing if it will crash and burn just before you need it? That is what Time magazine reported in their classic article “Why It’s Time to Retire the 40 IK.” See, when your money is in the market, timing can be more important than yields. If the market crashes down the home stretch, your dreams can go up in smoke.

It is not just Time magazine that sounded the warning. Just Google “the 40IK has failed,” and you’ll see that Time is not alone in their concern over the 40 IK. The sequence of returns risk should drive home that point.

Notice that both investors began with the same million dollars, took the same income, and had the same market results. The only difference is the order (sequence) in which the results came in. Investor A is dead broke in 14 years. Investor B had 14 years of income and still has almost 90% of his asset. So what is the difference between Investor A and Investor B? The flip of a coin. Timing. This shows us that pure luck or bad luck will determine your future. With a 40 IK, everything is outside of your control. Is that really the best system we can come up with? Do you want your retirement to come down to the flip of a coin? There has to be a better way, and there is.

The 401K Alternative

There is an alternative that is the chassis for three great ways to retire with no market risk, no hidden fees, and no taxation. It’s a plan that 22% of the top 1% of the wealthy use. It’s built upon an indexed life insurance policy. Why life insurance? For starters, life insurance is the last great tax break. You can retire with a lifetime of taxfree money, which means that you’ll also have access to your cash at any age with no tax penalty. Next, insurance is an industry built around reducing or eliminating risk, and this retirement plan is no different. The secret sauce, however, is the cap and the floor.

The cap means you’ll earn no more than the cap. Most plans are around 13 to 14%, although a few are uncapped with a spread. The real genius is the floor. With a floor at 0%, you’ll never lose a dime when the market tanks. Just to give you an example:

If you had $100,000 in the market in the year 2000 and you gained 100% of the S&P500 Index (which a 40 IK will never come close to doing 181% increase, and that is before taxes!

The product will produce a lifetime of tax-free income and more. You will also have a death benefit, should you die early, something a 40 IK will never offer. In addition, in the case of a major illness, such as a heart attack, stroke, or cancer, you can get an advance of up to 90% of your death benefit.

Let’s review the benefits:

• No risk of market loss

• No hidden fees

• Tax-free income for life

• Death benefit

• A lump sum for a major illness

• More money in retirement

Awesome Plan #2

The Five-Year Plan

All retirement plans have one major flaw in common. It takes a lot of time to build up a head of steam. Not just a lot of time, but a lifetime. However, with this specialized plan for six-figure earners, all premiums are made in the first 10 years. This plan uses other people’s money, or OPM (a loan), so the account has built up a full head of steam early on. Most people can only build a business using a loan, and a loan for retirement makes for one of the best plans you’ve never heard of. By applying a loan in the front end, you can secure a lifetime of a ton of money after paying premiums for only five years, while the lender pays premiums for 10 years.

The plan works like this. You pay premiums for five years only. The lender matches your premiums for five years and then doubles it for years five to 10. The lender pays $3 for every dollar of yours. Then in years 11 to 15, they get their money back with interest. Since the collateral for the loan is the policy, there is no risk for the lender and the loan will not affect your credit. By dumping in all the premiums within the first 10 years, the money grows at breakneck speed.

SEQUENCE OF RETURN RISKS Beginning Balance: $1,000,000

As an example, a 30-year-old male in good health will pay premiums of $20,000 a year for five years only. He will retire with an income of $207,000 per year from ages 65 to 90 and still have a life insurance policy with $ 1,2M in cash.

What if the market doesn’t do so well? The company also runs an illustration showing you how much you can retire with under a “Great Depression” scenario. Even there, you’ll retire with a six-figure income. It’s truly amazing how an account will grow when it’s impossible to lose any money.

Too good to be true? No, this product is offered by four different A-rated life insurance companies, which means they are monitored by your state as well. People trust life insurance because it is safe.

Awesome Plan #3

For Business Owners

This plan is a variation of the previous plan. It can be utilized for even more income and is a great way to shelter more money from taxes. It’s only available to business owners or their key personnel.

This method also uses a loan to front-load the policy as well, but the loan is run through the business. Follow the money. The business takes out an interest-only loan and then the business loans the money back to the owner. The owner then pays the interest-only payment back to the business. What you get is a tax break on the front end, since it’s a business loan and tax-free money in distribution. Yes, this is IRS-approved and tested. This plan requires your CPA to sign off on it, so someone you trust will vouch for the plan’s design.

When the owner retires and sells the business, the loan is repaid. It is a beautiful way to convert taxable profits to a tax-free income. It’s another safe way to retire with a lifetime of tax-free dollars and leave millions to your heirs.

In Summary

All three plans are built with safety due to the floor. All three will generate an income of tax-free money. All three leave tax-free money to your heirs in death, and tax-free money to you should you suffer a major illness. The first plan is perfect for your staff or those with a regular income. Plan #2 requires a sixfigure income in order to qualify, and Plan #3 is for business owners or key personnel. Since they are built upon a life insurance policy, health is a key issue, and will not be for everyone.

Any good financial plan will have its detractors on the internet. There is a lot of money flowing out of 40IK plans, and there are many with much to lose, so get a second opinion and let the numbers speak for themselves. Since all three plans are contracts, you’ll be able to see just how much of an income you can expect when you chose to retire, something no 40IK can do. Contact your financial planner and have a discussion. If they aren’t familiar with Plan #2 and Plan #3, have them contact me and I’ll bring them up to speed. It never hurts to get a second opinion.

And remember until you eliminate risk, you are not planning, you are hoping!

John Medwin is a Certified Financial Fiduciary and a retirement specialist with Forecast Financial in Winston Salem, NC. He's been helping clients reduce or eliminate risk, fees and taxes since 2006. He's licensed in 10 states and can be reached for questions or comments at [email protected]